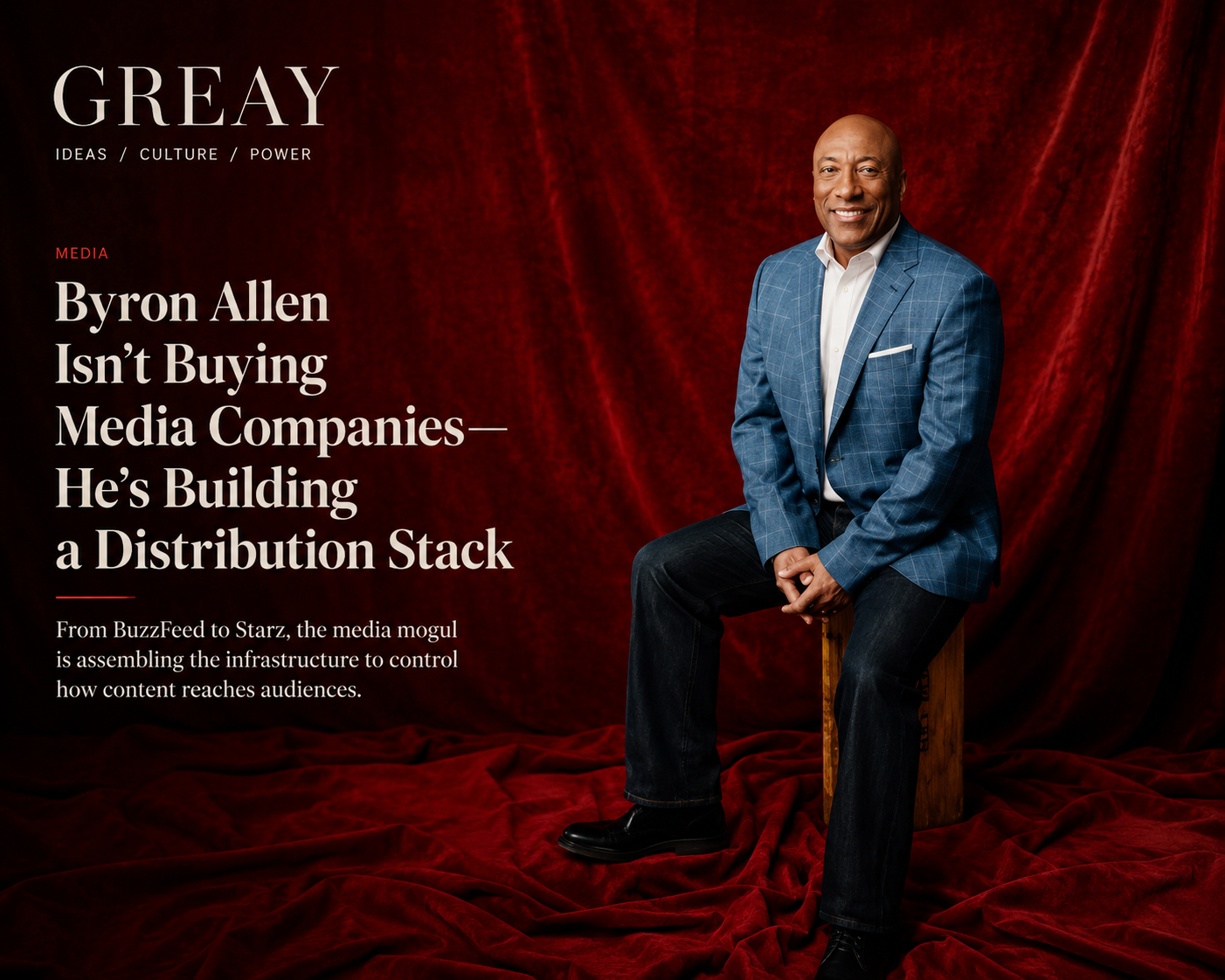

Byron Allen Isn’t Buying Media Companies — He’s Building a Distribution Stack

By DaMarko GianCarlo

For years, the media industry talked about fragmentation like it was the future.

Cable would die.

Streaming would replace television.

Digital publishing would replace traditional media.

Social platforms would become the new networks.

Advertising and subscription businesses would separate into entirely different ecosystems.

Everything was supposed to become smaller, faster, and disconnected.

But quietly, the industry has started moving in the opposite direction.

The real power in media is no longer just about owning content. It is about owning the pathways that move audiences between platforms, formats, and revenue systems. Distribution — not production alone — is becoming the center of gravity again.

That is why Byron Allen’s recent acquisition moves matter far beyond headlines about expansion or celebrity billionaire ambition.

On the surface, the portfolio can appear random:

local television stations, The Weather Channel, syndicated programming, a controlling stake in BuzzFeed, and now public interest in Starz.

But the logic changes once you stop looking at these companies as standalone brands and start looking at them as infrastructure layers.

BuzzFeed is not just a digital publisher.

It is traffic, ad inventory, social reach, audience behavior data, and cultural distribution.

Starz is not just a streaming platform.

It is subscription revenue, premium IP, licensing leverage, and direct consumer relationships.

Local television stations are not simply legacy assets.

They are regional distribution systems with advertising power and habitual audiences.

The Weather Channel is not merely weather programming.

It is one of the few remaining forms of daily appointment-based media behavior in America.

Syndicated programming is not glamorous, but it remains one of the most scalable economic engines in television.

Individually, these companies operate in different sectors.

Together, they begin resembling something else entirely:

a vertically layered media ecosystem.

That is the real signal behind Allen publicly emphasizing both AVOD and SVOD models.

Advertising-supported streaming and subscription streaming are often framed as competing systems. Allen appears to understand them as complementary ones. One captures mass reach. The other captures recurring revenue. One monetizes attention broadly. The other monetizes loyalty deeply.

Owning both means controlling multiple economic entry points into the same audience.

That is not simply expansion.

That is architecture.

For the past decade, technology companies trained the industry to believe aggregation was obsolete. Platforms prioritized infinite choice, isolated subscriptions, and fragmented viewing behavior. Consumers ended up juggling streaming services, social apps, creator ecosystems, newsletters, podcasts, FAST channels, and digital publications simultaneously.

But fragmentation created another problem:

distribution became unstable.

Audiences became harder to retain.

Advertising became less predictable.

Subscription fatigue accelerated.

Platforms lost cultural synchronization.

The more fragmented media became, the more valuable integrated systems started becoming again.

That is why companies across entertainment are now quietly rediscovering bundle logic — even if they no longer use the word “bundle.”

Amazon combines commerce, entertainment, cloud infrastructure, advertising, and logistics.

Apple combines hardware, services, payments, entertainment, and ecosystem lock-in.

YouTube is increasingly functioning as both a television network and creator economy infrastructure layer simultaneously.

The industry is not abandoning platforms.

It is rebuilding empires through interconnected systems.

And Byron Allen’s acquisitions increasingly resemble that same strategic philosophy.

What makes this especially significant is that Allen’s portfolio spans both old and new media economies at the same time. Most companies are trapped in one side of the transition. Legacy television companies struggle to modernize digitally. Digital-first companies struggle to build stable long-term revenue systems.

Allen appears to be positioning himself between both worlds:

traditional broadcast infrastructure and modern streaming distribution.

That matters because the next era of media may not belong to the company with the most content.

It may belong to the company that controls the most audience pathways.

The streaming era taught Hollywood how to distribute directly.

The next phase may be about reconnecting fragmented attention into controlled ecosystems again.

In that environment, distribution itself becomes the premium asset.

Not because consumers suddenly want cable back.

But because controlling how audiences move across media environments is becoming more valuable than owning any single platform alone.

The bundle never fully disappeared.

It simply fragmented into apps, platforms, subscriptions, feeds, and ecosystems.

Now the industry may be rebuilding it under different names.

And Byron Allen’s recent moves suggest he understands something many media companies are only beginning to rediscover:

content attracts attention.

Distribution compounds power.

Related Posts

What Happens When a Shoe Stops Explaining Itself

The Social Work of a Shoe

Michael Bublé Brings It Home in Rolex’s Most Intimate Documentary Yet

Time, Family, and Craft

Drake’s OVO Hits the Fairway: Streetwear Swagger Meets Callaway Precision

By Jayson Echo Drake’s OVO has officially taken its talents to the f

PlayStation Productions and Sony Pictures Unveil Full Trailer for Until Dawn Film Adaptation Ahead of Game’s 10th Anniversary

Sony Pictures and PlayStation Productions Drop Trailer for 'Until Dawn

PEPSI® Names Football Sensation Jack Grealish as Global Brand Ambassador in Multi-Year Collaboration

PEPSI® Names Jack Grealish as Global Brand Ambassador